This seems an appropriate time for me to revisit Alberta’s electricity system in search of a route to nuclear power in that province.

Alberta’s electricity system underwent radical changes since I wrote on a former government’s activities in 2017’s Alberta.Bound. In this post I’ll concentrate on data from the Alberta Electricity System Operator (AESO) in this post, mostly from their Annual Market Statistics data visualization which currently contains data from 2015 thru to June 2023. The AESO's data indicates rapidly declining potential for nuclear in the AESO’s market in recent years.

Alberta’s coal generators saw the wish for them to disappear grow for over a decade. In 2012 I wrote on the rapid opposition to federal regulations that would see emissions from new coal-power plants limited to something impossible with any operational technology, and a maximum lifespan of 50-years mandated, then, through emissions regulation, the goalpost essentially moved to 40 years within Alberta, and then a 2030 death data was mandated, and other generation sources incented. Alberta's Climate Leadership Plan (CLP) of 2017 noted the, "drive toward the development of 30 per cent of electricity generation capacity from renewable sources connected to the grid by 2030." [emphasis added] While the CLP itself spoke of efforts to remove, "policy barriers of the conversion of coal units to natural gas," many of the people that set policy had already created an understanding that ,"Two-thirds of the coal-generating capacity (4200 MW) will be replaced by renewable energy, and one-third (2100 MW) by natural gas."

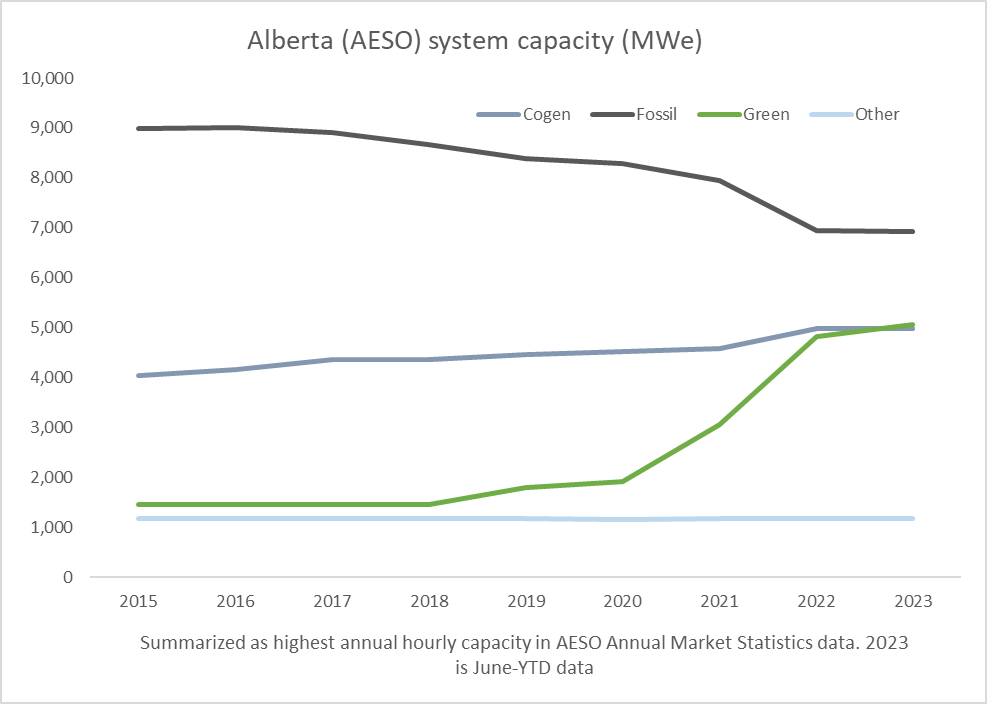

Summarizing the changes in generation capacity since 2016 by grouping fossil fueled generators together (gas, coal, dual fuel), “green” together (wind, solar and storage), displaying co-generation alone and lumping everything else in under “other” (including hydro), the decline in generating capacity of firm generators fueled by coal and/or gas is apparent, as is the, related, meteoric rise of “green” ones.

A couple of characteristics of these capacity groups help explain the great price increases Albertans have been exposed to in recent years. “Cogen” (for co-generation) has, never, in the entire data set, produced above 50% of its capacity, and rarely produces less than 25% of its capacity: 1 megawatt-hour (MWh) of cogen on the system is not the equivalent of 1 MWh of natural gas - or coal - in terms of flexibility. Much of the growing green capacity (wind’s 3,700+ MW and solar’s 1,200+ MWe) is dependent on weather. Alberta’s weather doesn’t cooperate in providing sunshine and wind when the grid most wants electricity. I refer to the ability of a source to contribute to meeting demand as capacity value, and for wind and solar in Alberta the capacity value continues to be near nil. For example, the hour of 6 pm this past February 23rd had one of the highest demands in the first half of 2023, but received only an average of 59 MW during that hour from 4,779 MW of wind and solar capacity. That’s not nothing - but it’s close! The shrinking amount of flexible, fossil fueled, generation gives the remaining flexible generators enormous pricing power, and the spark spread has therefore grown, from the meagre $6.82/MWh reported by the AESO for 2017 to an astonishing $124.46/MWh in 2022

The 2030 goals of eliminating coal from the electricity supply and having wind and solar at 30% of all generating capacity will both be met within the next 9 months. At what cost is not entirely clear as commensurate with those changes the cost per unit of electricity in Alberta has skyrocketed to become the most expensive in Canada.

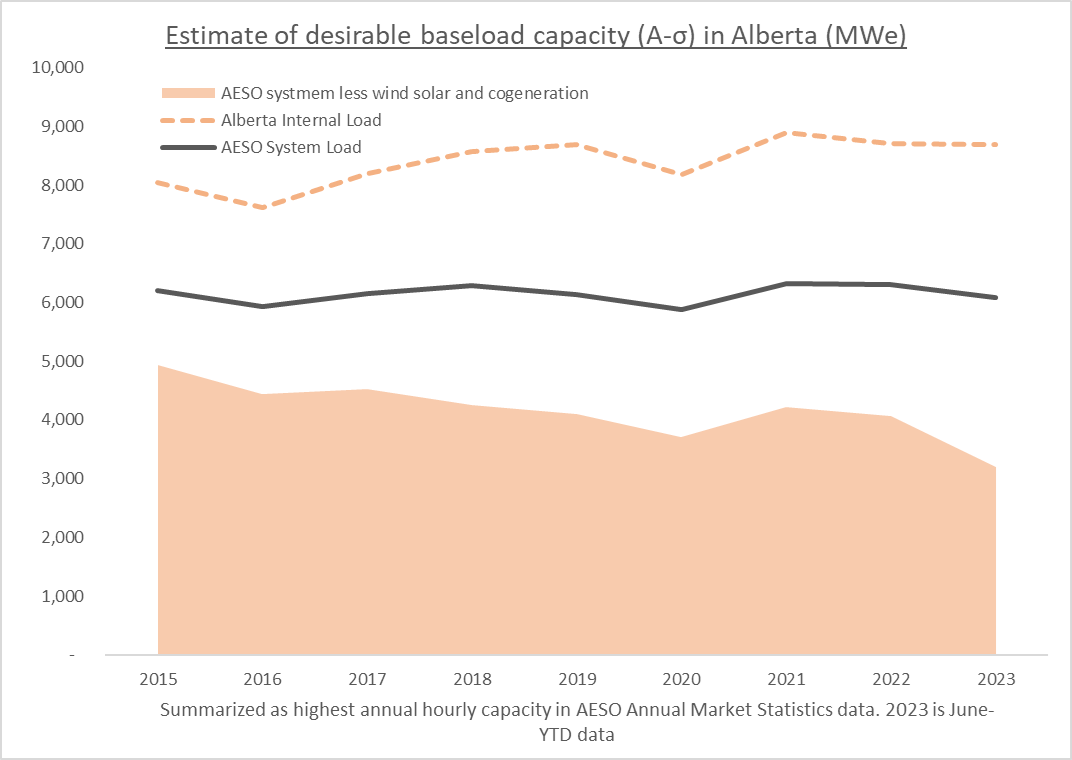

The supply mix impacts the prospects for nuclear, or any “baseload” supply that requires high capital spending that might be justified by low operating cost, and high capacity factors, over a long period of time. The German politicians that helped push Ontario’s Green Energy Act argued, not without reason, that nuclear and renewables were not compatible. Alberta’s market is not so large as it is often presented as many reports use an “Alberta Internal Load” (AIL) measure that includes the very significant, and growing, self-generation by Alberta’s energy-intensive industry. That self-generation is not counted in the AESO’s “system” load figures. I’ve argued the share of baseload most economical in a system is a function of the average load, and the variability of the load over a period of time, expressed as the mean less one standard deviation.The following graphic shows that theoretical “baseload” level for AIL, System (less self-generated supply), and then also without the wind, solar, and cogeneration producing on the system as all are essentially “must take” production.

The supply mix impacts the prospects for nuclear, or any “baseload” supply that requires high capital spending that might be justified by low operating cost, and high capacity factors, over a long period of time. The German politicians that helped push Ontario’s Green Energy Act argued, not without reason, that nuclear and renewables were not compatible. Alberta’s market is not so large as it is often presented as many reports use an “Alberta Internal Load” (AIL) measure that includes the very significant, and growing, self-generation by Alberta’s energy-intensive industry. That self-generation is not counted in the AESO’s “system” load figures. I’ve argued the share of baseload most economical in a system is a function of the average load, and the variability of the load over a period of time, expressed as the mean less one standard deviation.The following graphic shows that theoretical “baseload” level for AIL, System (less self-generated supply), and then also without the wind, solar, and cogeneration producing on the system as all are essentially “must take” production.

This analysis indicates the opportunity for baseload on the AESO system, after accounting for cogeneration and variable renewable energy systems, has shrunk over 1,700 MW, or about one-third, to 3,200 MW, in the past 8 years. The decline is mostly due to the addition of over 3,500 MW of wind and solar capacity over that period - and there’s far more to come. After Alberta’s government announced a short pause on approval of renewable energy projects at the province’s Utilities Commission, the Globe and Mail reported “3,400 megawatts of wind and solar projects currently under construction in Alberta.” This figure seems entirely plausible when compared with the system operator’s Connection Project Reporting, and the Utility Commission’s information on renewables. If no more renewables projects are approved Alberta’s grid might accommodate 2 CANDU EC6 reactors, or 4-5 GE Hitachi BWRX-300’s - but there is already 2,500 MW more capacity, mostly solar, seeking approval from the Utility Commission. If all projects before the Commission enter service alongside all those existing or under construction, Alberta will have over 9,000 MWe of wind and solar capacity, which exceeds the maximum annual peak load in the province.

The rise in renewables has been driven by policy changes that proponents present as allowing the power of the market to work, with the market choosing renewables, but could better be described as manipulating a system to produce a desired outcome. Alberta has long accommodated power purchase agreements (PPA’s) allowing a renewable generator to connect to the grid while pre-selling all their output to an entity in advance, as well as making the province friendly to cogeneration with a significant share of industry needing heat and being capable of producing excess electricity while doing so. As Canada has pushed into carbon pricing and attempting to prevent the flight of industry due to leakage, one tool that became useful was only charging for carbon emissions above a certain level for an industry - or more complicated comparator. A federal regime exists, but provinces can negotiate their own solutions, and Alberta has.

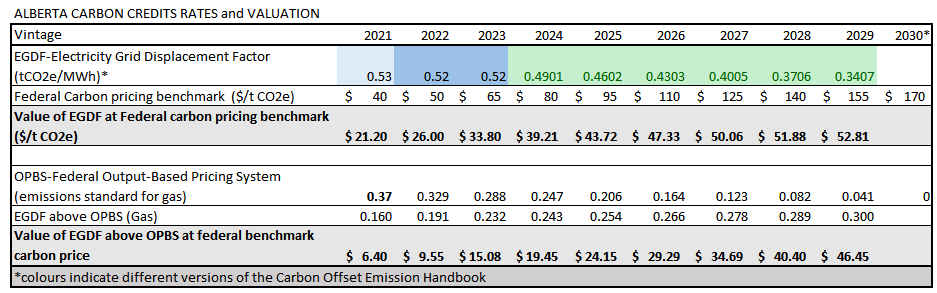

The steep increase in the AESO's pool price should, in basic market theory, ebb the decline of frim capacity by attracting new entrants into the market, but the federal government is threatening to essentially end gas-fired generation by 2035 so it’s unlikely that will happen (beyond once CCGT facility set to enter service in the near future). Two features of the newish policies in Alberta are an “Electricity Grid Displacement Factor” (EGDF) and the Technology Innovation and Emissions Reduction (TIER) Regulation. The first sets the amount of emissions that will be given to wind and solar generators that they may sell them to other industry within Alberta - most notably the oil sands operators. This all gets far too complicated very quickly, but as I understand it the credits are set at levels depending on how a project is situated, and when the generator officially enters the program, and will exist for at least 8 years, but may be going to 10 and can be extended beyond that. The EGDF’s are generous, exceeding what would be justified using the federal Output-Based Pricing System (OBPS). I won’t dwell on this pricing beyond offering the following estimates of the monetary benefit per megawatt-hour of production from wind and solar, under Alberta’s EGDF credits, compared to what might be a rational credit under the federal Output-Based pricing system (based on avoiding supply from that system's declining exemption for gas-fueled generation), and valuing the EGDF, and variance to OBPS, at the federal carbon price (in lieu of a better estimate for the value of credits under Alberta’s TIER system).

Were nuclear to be put on the carbon credit playing field, there’d still be a problem in that the credits are basically structured to fund wind and solar during the period the output the output of those generators may back back their capital costs. New nuclear needs cost guarantees out beyond the 8-10 years that suffice for the shorter-lived renewables facilities. The growth of wind and solar in Alberta, far above anywhere else in the country, is not due to a market working, but a market being worked.

Gaming the market design to favour wind and solar has provided another benefit to those generators. This benefit is directly proportionate to the harm to consumers in escalating prices on the AESO market. From less than $23/MWh in 2017 the average price (weighted to system load) rose sharply to where it now sits above $150/MWh. The price jump in the AESO’s annual 60 million MWh system equates to well over $7 billion. There are multiple contributors but the main reason for large price changes is pricing power frequently exists for suppliers due to heightened demand and or declining supply. More information on pricing power can be found in Market Surveillance Administrator reporting, including, "Some larger suppliers continued to exercise market power... One supplier withheld a large amount of capacity by pricing it above $900/MWh regardless of market conditions."

If the plan is simply for more of the same, the AESO’s market is not sustainable and would be unattractive to any generation not anticipating high out-of-market payments (such as through environmental attributes such as the EGDF/TIER model)

But…

While the AESO’s market system provides little opportunity for nuclear, self-generation/cogeneration offers some hope. Co-generation has been defined as, "The simultaneous production of electricity and another form of useful thermal energy used for industrial, commercial, heating or cooling purposes."(AESO 2017LTO) In Alberta it has been driven higher by the oil industry, which needs, "more heat than power, and it’s this heat that creates the surplus power potential that could be exported to the grid.

As cogeneration is industrial it presents much more as “baseload” supply - meaning relatively constant generation with low levels of variability. Using the same average less one standard deviation equation for an economic “baseload” share, the opportunity for nuclear in cogeneration now exceeds the opportunity in the AESO’s troubled market, and that difference will only grow. Were cogenerators to move to such a reactor their natural gas use would plummet along with their need to purchase emission rights under the TIER system - a system which may well then credit industries for reducing emissions to new lows., including the main one extracting oil from sand.

But…

While the AESO’s market system provides little opportunity for nuclear, self-generation/cogeneration offers some hope. Co-generation has been defined as, "The simultaneous production of electricity and another form of useful thermal energy used for industrial, commercial, heating or cooling purposes."(AESO 2017LTO) In Alberta it has been driven higher by the oil industry, which needs, "more heat than power, and it’s this heat that creates the surplus power potential that could be exported to the grid.

As cogeneration is industrial it presents much more as “baseload” supply - meaning relatively constant generation with low levels of variability. Using the same average less one standard deviation equation for an economic “baseload” share, the opportunity for nuclear in cogeneration now exceeds the opportunity in the AESO’s troubled market, and that difference will only grow. Were cogenerators to move to such a reactor their natural gas use would plummet along with their need to purchase emission rights under the TIER system - a system which may well then credit industries for reducing emissions to new lows., including the main one extracting oil from sand.

Problems for nuclear in cogeneration are substantial, both technically and politically.

Technically the products need to be both heat/steam and power. This is not generally done with nuclear reactors - certainly not with the CANDUs Canada has developed. But there are many new designs of reactor, including one from Terrestrial Energy, a firm that’s built a presence in Alberta promising, “Carbon-Free Energy for Global Industry.” Building a first-of-a-kind reactor is not an experience many wish to embrace, and it’s one that’s not gone well in Europe or North America for many decades. The initial project would require government support.

Politically, in the sense of the exertion of power, the current system is essentially set up so that renewable generators are gifted the rights to sell emissions, and it is expected the oil and gas industry will buy those rights under TIER as long as the system offers a cost savings compared to Canada’s carbon pricing. Economically that's sensible if it's cheaper to lower emissions in electricity, but as we've seen it's not been cheaper for consumers at all, and does not look to be sustainable. Beyond fiscal concerns, the current EGDF/TIER setup is a system where the bad oil and gas companies are to gain enough social license to operate so long as they recite land acknowledgements and ESG commitments while paying an indulgence to the good wind and solar generators (in some cases the same company). That strikes me as no more sustainable for the industries purchasing emissions than adding wind and solar as quickly as possible while consumer rates skyrocket does for the electricity system.

https://istanbulolala.biz/

ReplyDeleteYKNF20

urfa evden eve nakliyat

ReplyDeletemalatya evden eve nakliyat

burdur evden eve nakliyat

kırıkkale evden eve nakliyat

kars evden eve nakliyat

U3Y

B8DA2

ReplyDeleteBolu Şehirler Arası Nakliyat

Trabzon Parça Eşya Taşıma

Çerkezköy Çamaşır Makinesi Tamircisi

Keçiören Fayans Ustası

Ünye Boya Ustası

order testosterone propionat

Batman Şehir İçi Nakliyat

https://www.anabolickapinda16.com/

Ünye Organizasyon

43BC8

ReplyDeleteBatman Evden Eve Nakliyat

Zonguldak Lojistik

Afyon Evden Eve Nakliyat

Denizli Lojistik

Bonk Coin Hangi Borsada

Eskişehir Lojistik

Gümüşhane Parça Eşya Taşıma

Bibox Güvenilir mi

Kastamonu Şehir İçi Nakliyat

F30F0

ReplyDeleteZonguldak Lojistik

Tekirdağ Cam Balkon

Denizli Parça Eşya Taşıma

Batman Şehirler Arası Nakliyat

Ardahan Şehir İçi Nakliyat

Çorum Evden Eve Nakliyat

Bitlis Lojistik

Trabzon Şehirler Arası Nakliyat

Tokat Şehirler Arası Nakliyat

27952

ReplyDeleteTunceli Şehirler Arası Nakliyat

Kütahya Parça Eşya Taşıma

Altındağ Fayans Ustası

Çerkezköy Yol Yardım

Bolu Parça Eşya Taşıma

Isparta Parça Eşya Taşıma

Bolu Şehirler Arası Nakliyat

Ardahan Şehir İçi Nakliyat

Tekirdağ Parça Eşya Taşıma

BDB62

ReplyDeleteKırklareli Parça Eşya Taşıma

Niğde Lojistik

Isparta Parça Eşya Taşıma

Sakarya Şehirler Arası Nakliyat

Çerkezköy Kombi Servisi

Adana Şehirler Arası Nakliyat

Elazığ Parça Eşya Taşıma

Bitlis Parça Eşya Taşıma

Nevşehir Lojistik

7D13A

ReplyDeletereferans kimliği nedir

binance referans kodu

referans kimliği nedir

binance referans kodu

resimli magnet

binance referans kodu

resimli magnet

resimli magnet

binance referans kodu

9F01B

ReplyDeletebitexen

huobi

binance referans kimliği

gate io

toptan mum

referans kodu binance

kraken

binance

mexc

D4A60

ReplyDeletehuobi

bybit

binance referans kod

4g proxy

huobi

filtre kağıdı

paribu

kripto para telegram

bitget

F4041

ReplyDeletemobil 4g proxy

telegram kripto grupları

kaldıraç nasıl yapılır

referans kodu

referans kod

kucoin

2024 Calendar

bitcoin hesabı nasıl açılır

June 2024 Calendar

5BEB05ACAA

ReplyDeletekiralık hacker

hacker arıyorum

kiralık hacker

hacker arıyorum

belek

1BAA20AB68

ReplyDeletehacker bul

hacker bul

tütün dünyası

hacker bul

hacker kiralama

2AC5E0F0E8

ReplyDeleteTakipçi Satın Al

M3u Listesi

Coin Kazanma

Razer Gold Promosyon Kodu

Türkiye Posta Kodu