I did write a post a year ago with 6 suggestions for the then-new Premier’s government. Reviewing the list now I see some action on 4 of the points. One exception remains “Restrict eligibility to the Industrial Conservation Initiative (ICI).” In terms of what can be done within today’s system my comments from last year remain my short-term position on industrial electricity prices:

Purging the ICI rolls of all entities with no actual exposure to trade will offer an immediate reduction in residential, and small business, electricity costs.

This would have an immediate benefit for smaller industrial consumers that are not eligible to participate in the ICI. The reality for existing industrial consumers within the ICI is that they have been largely protected from rate increases with a program promoting inefficient spending that only benefits ICI participants by adding to the burden of remaining Ontario consumers. Lowering rates further should be an outcome from lowering the electricity sector’s costs - not transferring costs to lesser consumer classes, most of which subsequently transferred costs onto future ratepayers and taxpayers.

The Market Renewal Initiative was the last government’s hope for future cost reductions, and there’s no indication today’s Ford government has changed tack. There’s a lot of fine analysis being done on different aspects of a new market design, and very informative reporting being produced. It’s just not clear, to put it very kindly, that there is a real commitment to a market system.

In the beginning (of the current structure) there was the Independent Electricity Market Operator (IMO), and its market, and maybe it was good for an hour or two but things went sideways pretty quickly.

A quick review of what a market is. Very quick. From the first paragraph of the Wikipedia entry:

It can be said that a market is the process by which the prices of goods and services are established. Markets facilitate trade and enable the distribution and resource allocation in a society. Markets allow any tradeable item to be evaluated and priced.

Ontario sent the market sideways shortly after it opened in May 2002 by freezing prizes, which had experienced spikes due to supply being tight. The freeze discouraged new suppliers, so by 2005 a newer government was introducing what was referred to as a “hybrid market”, featuring the creation of a true-up mechanism called the global adjustment. The new surcharge allowed the system to go to Ontario consumers at the end of the month to collect the difference between what the market collected for supply, and what supply actually cost. To emphasize the change in the role of a market in the system, the Independent Electricity Market Operator (IMO) became the Independent Electricity System Operator (IESO).

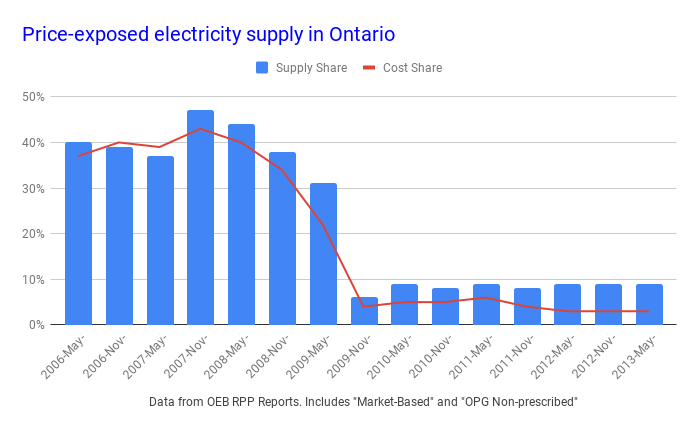

For a number of years we can see the deterioration of the market through the Ontario Energy Board’s Regulated Price Plan (RPP) reports which were released twice each year. That RPP report predicts what the cost of supply will be in the coming rate period (and adjusts for variances in past periods).The methodology in the RPP reports provided some insights. Two categories of generators had some exposure to market pricing: “Market-Based” generators received only the Hourly Ontario Energy Price (HOEP) revenue, and “OPG Non-prescribed generators” (coal and most hydro-electric facilities) had a revenue cap which meant they’d need to return revenues if the average selling price exceeded a set amount, but they had motivation to average the full capped rate.

In 2009 most market exposure ended with the collapse of demand during the recession, and with it the hybrid market’s pricing (HOEP). Ontario Power Generation (OPG) received fixed cost contracts to keep coal-fueled generators operating, and private hydro generators were given 20-year HESA contracts. By 2010 the only generators depending on revenue from selling into the IESO’s “market” were importers and the non-regulated hydro facilities of the OPG (the public generator).

The last time the OEB RPP reports showed the share of “Market-Based” supply was for the May 2013- October 2013 rate period. Shortly after that report was published two giants of Ontario electricity cost analysis had an article in the Financial Post titled [OPG] turning water into debt:

The big lag on OPG’s earnings has been the unregulated hydroelectric segment. It contributed more than $500-million or 46% of OPG’s pre-tax generation in 2008. Now it loses money. The reason for the loss is simple: OPG’s non-regulated hydro-electric assets are the only significant generation in Ontario exposed to the market price of electricity, which has collapsed under the McGuinty Liberal green energy manipulations.

The argument was convincing enough that the government altered regulations so all OPG hydroelectric facilities would receive regulated rates. With the exit of that small share of “market-based” supply the OEB dropped reporting on the “Market-based” share of total supply.

What remained of supply exposed to market pricing was almost entirely imports. The government effectively directed the IESO to kill this last remaining instance of supply exposed to a market-based pricing by ordering a contract for supply from Quebec.

That’s the sellers side of the market. The IESO did not design the massacre, but having swallowed the Ontario Power Authority the collective personnel of the current IESO were the executioners.

The buyers side of the so-called market is not much better. A Day-Ahead Market High-Level Design describes the current Day-Ahead Commitment Process (DACP) from the load perspective:

In Ontario, only a relatively small portion of load market participants currently submit their own bids into the DACP or the RTM. These load market participants include dispatchable loads (DLs) and hourly demand response (HDR) resources. There is a third class of load market participants called non-dispatchable loads (NDLs)...According to the regulator’s Market Surveillance Panel, the only thing demand response resources do is file into the DACP:

The Panel continues to question the value of [Demand Response auctions] for ratepayers, given that none of the hourly demand response resources have been activated to provide DR and reduce their consumption.The “third class”, after dispatchable loads and DR, comprises most load/demand as it includes Local Distribution Companies (LDC’s). LDC’s cannot currently purchase supply, “due to regulatory barriers for local distribution companies (LDCs) to take on financial positions for their load customers.” (page 16).

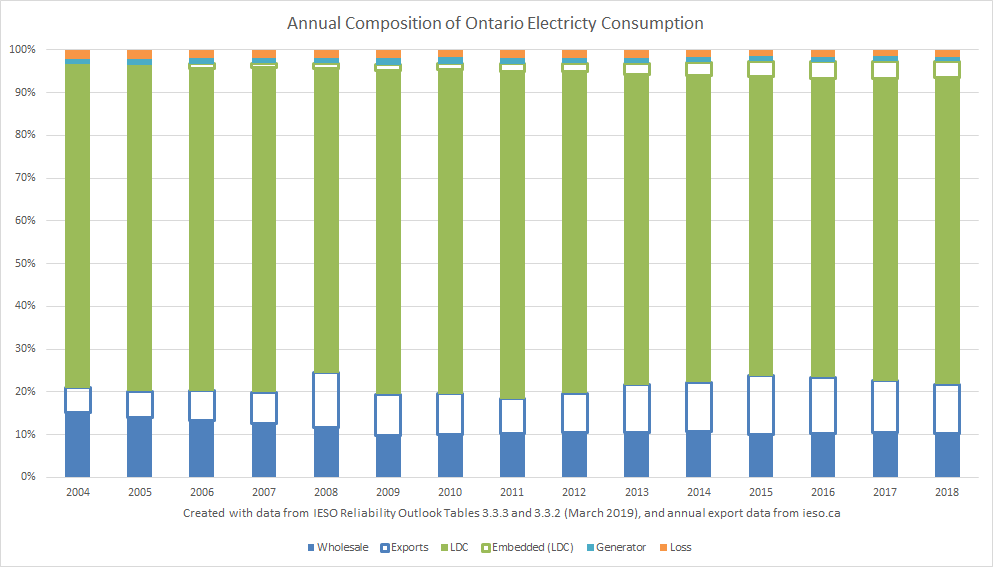

A view of annual composition of consumption, or the buyers’ side of the market, shows limited possible active wholesale market participation. Since 2011 the largest class of consumer actually active in purchasing from the market directly is exporters.

The combination of high supply with no price exposure to the market, and essentially no ability to purchase supply at a market price within Ontario (due to the global adjustment surcharge) is driving exports at very low prices.

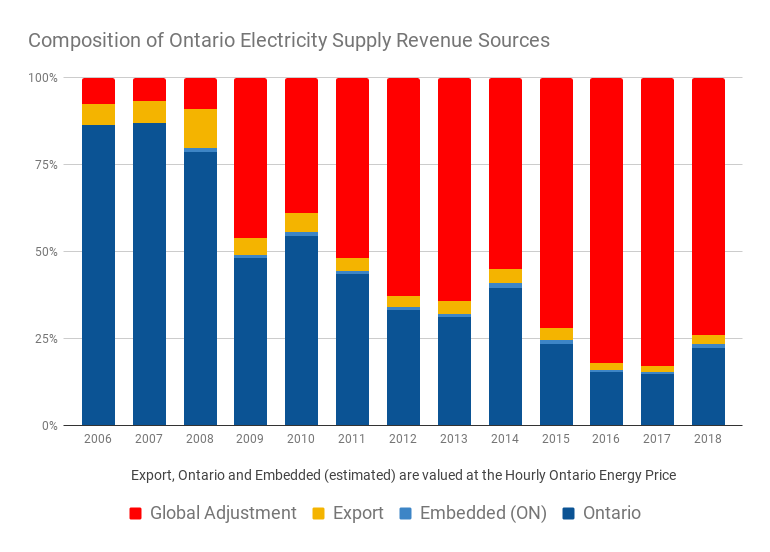

The annual composition of revenues may be the best indicator of the health of the market. In the early years of the current hybrid design most revenues came from sales into the market, while in recent years as little as one-fifth of the revenue is from sales into the market.

That’s the context in which I view the government asking what can be done about industrial electricity pricing. It seems a distraction to the bigger question of what to do about the broad system.

The IESO, and the Ministry of Energy, have promised middling savings from “Market Renewal.” $3.4 billion over a 10-year period sounds significant, unless one views in as $340 million a year at a time when the system is borrowing $2.7 billion a year under [un]Fair Hydro Plan, with the current Premier having been elected on cutting prices 12% more than the last ban plan did.

“Renewal” is not the task. The hybrid market structure Dwight Duncan created back in 2005-05 does not need a new hairstyle, or a pedicure, or a weekend at a spa, or a sabbatical to learn something new at a foreign school. The little blips of market revenue are traces of a past life - artifacts from fuel costs and water taxes that were but elements of a former being.

The condition of the hybrid market (think of it as “E”) described;

'Is metabolic processes are now 'istory! 'E's off the twig! 'E's kicked the bucket, 'e's shuffled off 'is mortal coil, run down the curtain and joined the bleedin' choir invisible!! THIS IS AN EX-[MARKET]!!”Nobody wants to throw the baby out with the bathwater, but I feel obliged to point out the IESO is hanging around with a dead baby.

The IESO’s roadmap for “renewal” calls for more markets and/or auctions:

- a day-ahead market (DAM),

- a real-time balancing mechanism (Enhanced Real-Time Unit Commitment Engagement), and

- A mechanism to procure the firm capacity need to have supply available at all times it is demanded (Incremental Capacity Auction).

The day-ahead market is the main arena for trading power. Here, contracts are made between seller and buyer for delivery of power the following day, the price is set and the trade is agreed.The reason I delivered an historical background focused on supply, and purchase, issues is because they seem to be ignored at the IESO. While there’s a wealth of terrific information at the IESO site on the structures to be created in their “renewal” plans, there’s practically nothing on producing sellers and buyers with skin in the market game - ones that can actually control costs, and generate profits, by participating in the IESO’s DAM thing.

…

Daily trading is driven by the customers’ planning. A buyer, typically a utility, needs to assess how much energy (‘volume’) it will need to meet demand the following day, and how much it is willing to pay for this volume, hour by hour. The seller, for example the owner of a hydroelectric power plant, needs to decide how much he can deliver and at what price, hour by hour. These needs are reflected through orders entered by buyers and sellers into the Nord Pool day-ahead trading system.

Briefly returning to the Industrial Conservation Initiative - because it was a request for an opinion on industrial pricing that started me writing this - I should emphasize the ICI depends on a dysfunctional market: it only shifts supply costs because today’s dead-baby market doesn’t recover most costs.

The IESO appears conditioned to seize each opportunity to make poor decisions. One example is forecasting wind output centrally within the IESO. It’s a wildly inappropriate task for a market operator. Is industrial wind some special needs child that can’t function on its own? It’s time to kick the brats out of the IESO’s house to see if they can function on their own.

What about contracts?

I’ll come back to that.

An example of the IESO’s avoidance of decision-making on the demand side:

In other jurisdictions, load serving entities (LSEs) and load retailers are responsible forbidding on behalf of their [non-dipatchable load (NDL)] customers. LSEs and load retailers take on this responsibility because they are the entities responsible for securing supply for their load customers. Ontario is not in a position to achieve such active load participation due to regulatory barriers for local distribution companies (LDCs) to take on financial positions for their load customers. (pg 15)When I read that 6 months ago I empathized with the IESO’s predicament in designing a market within the constraints of existing regulation. I’ll return to argue the government must make changes required for a market after I’m done with the IESO.

Shiny things.

Almost to the day the IESO was releasing the DAM high-level design document another arm of it released Removing Obstacles for Storage Resources in Ontario. Storage is one of those exciting trendy topics I’ll group into a category of shiny things. Where shiny things are involved the first four recommendations from the IESO were, and I quote:

- Review and amend Market Rules

- Review the Ontario Energy Board Codes

- Consider energy storage in Ontario legislation and regulations

- Consider the market-efficiency impact of applying wholesale uplift charges

“IESO CEO sheds light on importance of preparing for a high-DER [distributed energy resources] future” was a news update from the organization this week citing a new report from the ignominious “Energy Transformation Network of Ontario.” You are excused for not knowing the group is ignominious as they rebranded from the Smart Grid Forum moniker it was using back when Ontario was probably the worst in the world at providing value to end-consumers with then-shiny meter and billing technology.

The new ETNO report opens:

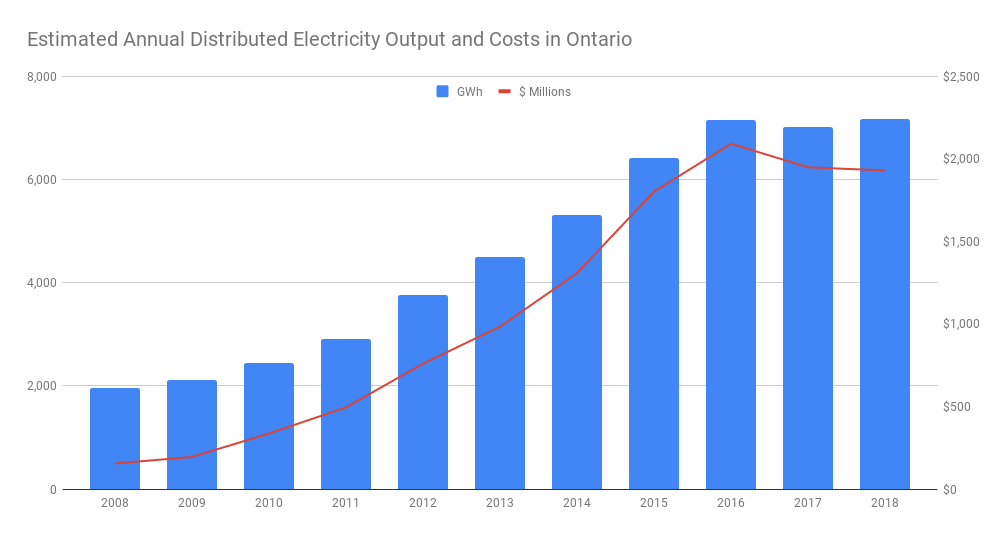

A reliable, affordable and resilient electricity system is essential to Ontario’s prosperity. Like other sectors, electricity is undergoing significant disruption, as the combined forces of decentralization, digitization and democratization take hold. In particular, small-scale, distributed energy resources (DERs) – such as combined heat and power (CHP), solar, energy storage and wind – are growing rapidly, thanks to decreasing technology costs, consumer trends and public policy. In Ontario, at least 4,000 megawatts (MW) of DERs have been contracted or installed in the last 10 years. This does not include an unquantifiable amount of load control, behind-the-meter energy storage and demand-response capacity that can also be regarded as DERs.4,000 MW exist because 3,391.4 MW were added due to public policy(pdf). The IESO executed this policy, delivering unnecessary supply at spectacularly high prices - although that would be hard for most people to know as the IESO seldom report on either the output or costs of the contracts they hold. I estimate from 2008 to 2018 the DER contracting added 5.2 terawatt-hours (TWh) and increased annual supply costs $1.774 billion.

I’d be happy to be corrected on the figures - stunned if, at an average cost of 34 cents/kWh in a time of excessive supply demonstrated by dead baby market pricing, massive dumping on export markets and staggering curtailment, the growth in DER’s wasn’t the electricity policy with the worst value-proposition on the planet. The only signal for the future of that experience is that the IESO is capable of implementing extremely poor policy.

The news still gets worse. On June 6, 2019 the IESO published an Operability Assessment to 2025. This is complex stuff, but I hope we get the gist of it from these quotes:

The Most Severe Single Contingency (MSSC) ... refers to generation capacity lost due to a single forced outage of generation or transmission equipment. It is one of the quantities used to determine the amount of operating reserve the IESO schedules for each dispatch interval…

Traditionally, the [IESO controlled grid (ICG)]’s MSSC was mainly determined by the largest generation unit (one unit at Darlington NGS, approximately 900 MW) that could be lost…

Projections for 2025 show the potential for 3,160 MW of [Distributed Energy Resources DERs)] (total installed capacity), which could generate up to 2,600 MW during high output conditions, being in service in Ontario. The majority of DERs follow the IEEE 1547 standard for Interconnecting Distributed Resources with Electric Power Systems, issue 2003, which requires them to disconnect as soon as voltage or frequency is outside the normal ranges…

...Further analysis showed that a severe transmission fault within the 500 kV system that results in the loss of a Darlington NGS unit would also lead to an additional loss of about 2,000 MW of DERs with a coincident high output of around 1,700 MW, representing a total potential generation loss of about 2,600 MW…

What is it telling us? Under certain operating conditions, the insufficient voltage and frequency ride-through capabilities of the majority of DERs could result in a large-scale loss of output. That will require the IESO to plan for new and very large MSSCs.

The DERs contracted over the past decade (mostly solar, but with significant amounts of wind) are yet more special needs offspring putting even more of a stress on the rest of the electricity family.

The IESO needs to get past its obsession with shiny things. There have been very good arguments that regulations need to change to allow entities to both suppliers and consumers be - to paraphrase the Bard - but there is no sanity in targeting specific technologies for preferential treatment.

There would be logic in removing the preferential treatment that technologies now receive, but the IESO cannot do that. My opinion is that there is expertise in the IESO to do smart things with market design but it is unlikely to thrive if the body does not jetision the obsession with shiny things that prevent a clear view of what is required to succeed with a market within an organization that should be defined by its past failures with a market.

While the case is pretty strong that good market design can provide better value than ours has, I think the case has not been made that energy markets clearly outperform regulated monopolies for consumers in either the traditional sense or in the delivery of low-emission systems. But if we are to go with a market system, despite the failed efforts of the past two decades in trying to do so, then we should try to do that well.

I won’t pretend to know how to implement a market design, but I will speculate on what eggs need to be broken to do so:

The Ford government has backed out of a provincial cap and trade regime and opposes a federal price on greenhouse gas emissions. It has, understandably, claimed Ontario has done its part in reducing emissions. I respect that, having done analysis measuring different supply mixes by the implied cost of carbon. To demonstrate this, I’ll return to $340/MWh for the distributed energy resources contracted over the past decade: the implied cost of carbon needed to justify those contracts is roughly $851 per tonne of CO2e - which is much more than the federal price being opposed (to be $50/t CO2e). My point is the government is probably right to oppose paying more in specific CO2 pricing as we already are paying through our electricity supply decisions, but it would be wrong to avoid the use a social cost of carbon in determining stranded assets.

We should be as cognizant of the 1993-2003 experience as we are with the last decade’s. During that period prices were frozen, to protect consumers, costs cut at the public utility - to protect consumers - leading to poor generator performance, eventually idling 8 nuclear units, and ramping up coal use to compensate for the deterioration of the rest of the system. By 2003 all parties had policies for cleaner air through the elimination of coal in generating electricity. We do know how to control costs in a way that harms our local environment, but that should not be our model for controlling costs.

So here’s my recommendation for a durable industrial rate policy:

Market Renewal is a term that demonstrates an ignorance about the current state of an electricity market in Ontario.

The market is dead.

What is needed is not renewal, but re-animation.

Notes:

I did jot down some answers to questions the government asked on industrial pricing, but did not submit them.

Link to the spreadsheet with graphic for Distributed Generation and costs

Link to sheet with Composition of Ontario Supply Revenue graphic

There would be logic in removing the preferential treatment that technologies now receive, but the IESO cannot do that. My opinion is that there is expertise in the IESO to do smart things with market design but it is unlikely to thrive if the body does not jetision the obsession with shiny things that prevent a clear view of what is required to succeed with a market within an organization that should be defined by its past failures with a market.

While the case is pretty strong that good market design can provide better value than ours has, I think the case has not been made that energy markets clearly outperform regulated monopolies for consumers in either the traditional sense or in the delivery of low-emission systems. But if we are to go with a market system, despite the failed efforts of the past two decades in trying to do so, then we should try to do that well.

I won’t pretend to know how to implement a market design, but I will speculate on what eggs need to be broken to do so:

- the government needs to update regulations, and those updated regulations will devalue existing contracts;

- generators are going to need to bid supply into the day-ahead market, and they are going to need to have to make up for not delivering on their bids in a spot market - simply getting paid for what is produced whenever it is produced has to be illegal: pay the contracted rate on what can be guaranteed by the producer in the DAM. While wind should be seen as a target of those comments, embedded solar should too: this is not a product any willing buyer would go anywhere near.

- There needs to be a pathway to new entities that can make embedded solar a viable product - individual solar facilities will need to sign on with aggregators which will have the capability to operate in a market.

- Nuclear operators with unplanned outages are also going to have to find sellers in the spot market to meet their delivery commitment (or face stiff penalties)

- The Industrial Conservation Initiative must end - the behind-the-fence/meter generators current participants have invested in will have real value in an Incremental Capacity Auction (unlike the substantial private value they currently provide at the expense of real systemic value)

The Ford government has backed out of a provincial cap and trade regime and opposes a federal price on greenhouse gas emissions. It has, understandably, claimed Ontario has done its part in reducing emissions. I respect that, having done analysis measuring different supply mixes by the implied cost of carbon. To demonstrate this, I’ll return to $340/MWh for the distributed energy resources contracted over the past decade: the implied cost of carbon needed to justify those contracts is roughly $851 per tonne of CO2e - which is much more than the federal price being opposed (to be $50/t CO2e). My point is the government is probably right to oppose paying more in specific CO2 pricing as we already are paying through our electricity supply decisions, but it would be wrong to avoid the use a social cost of carbon in determining stranded assets.

We should be as cognizant of the 1993-2003 experience as we are with the last decade’s. During that period prices were frozen, to protect consumers, costs cut at the public utility - to protect consumers - leading to poor generator performance, eventually idling 8 nuclear units, and ramping up coal use to compensate for the deterioration of the rest of the system. By 2003 all parties had policies for cleaner air through the elimination of coal in generating electricity. We do know how to control costs in a way that harms our local environment, but that should not be our model for controlling costs.

So here’s my recommendation for a durable industrial rate policy:

Identify stranded assets. The revenue to retire those assets should be recovered from residential ratepayers and their public institutions (the MUSH sector). Trade-exposed industry should be excluded from the tariff retiring the stranded assets in Ontario as demonstrated by Germany’s current EEG (Renewable) surcharge model.Controlling industrial electricity rates should not be planned as coming at the expense of other consumers - as it now is. It would be unfortunate if concern for industrial rates overshadowed the moves in desperately necessary market design.

Market Renewal is a term that demonstrates an ignorance about the current state of an electricity market in Ontario.

The market is dead.

What is needed is not renewal, but re-animation.

Notes:

I did jot down some answers to questions the government asked on industrial pricing, but did not submit them.

Link to the spreadsheet with graphic for Distributed Generation and costs

Link to sheet with Composition of Ontario Supply Revenue graphic

Link to sheets with Price-exposed electricity supply in Ontario graphic

Link to excel workbook with Annual Composition of Ontario Electricity Consumption graphic

Thank you for sharing Energy Analysis in UK

ReplyDeleteA3D32F6A65

ReplyDeletetakipçi alma

small swivel accent chair

8CFC3B9E

ReplyDeletekemer esçort

esçort bayan balıkesir

antalya esçort numaraları

ereğli esçort

ataşehir yabancı esçort

gaziantep rus esçort

ataşehir olgun esçort

burhaniye esçort

yalova esçort

1F472A5C

ReplyDelete随机聊天

Bate-papo aleatório

Chat aleatoriu

Random Chat

미트플라이랜덤 채팅

Willekeurige chat

chat casuale

แชทแบบสุ่ม

Náhodný chat