Privatized generators are to see price reductions as the public generator's pricing soars

Ontario’s electricity system operator recently announced a Northern Hydro Program (NHP), calling it, “another critical component to the IESO’s strategy to meet unprecedented forecasted demand through the use of the Resource Adequacy Framework.”

The NHP will secure over 1,000 megawatts from approximately 26 large, hydroelectric generating facilities in Northern Ontario, providing considerable value for ratepayers with expected savings to re-contract facilities at rates 20 per cent below those under previous contracts compared to extending current contract terms. The program is intended to support the continued operation of these facilities with new 20-year contracts…

This news, while positive, is not as clear a win for ratepayers as it appears. The hydro sites to be re-contracted, under the NHP, are those contracted under a previous program known as the Hydroelectric Contract Initiative (HCI). A little over 6 years ago, the IESO posted a directive on the wind-down of the HCI program, noting, “The HCI program is the IESO’S last active electricity generation procurement program. The HCI program allowed existing hydroelectric facilities without electricity contracts to obtain 20-year contracts…”

The HCI-to-NHP transition isn’t the first re-contracting of the gluttonous green energy procurements that occurred around 2010, but they may be the first 20-year extensions.

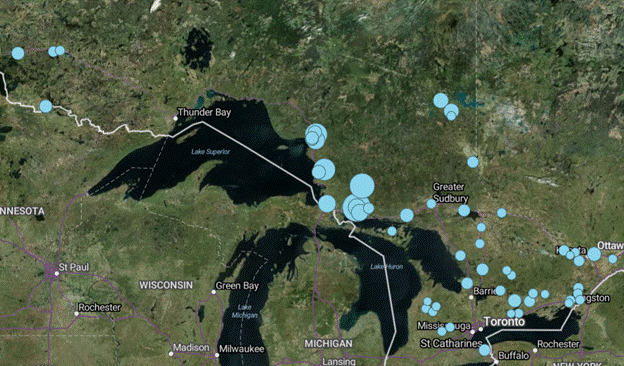

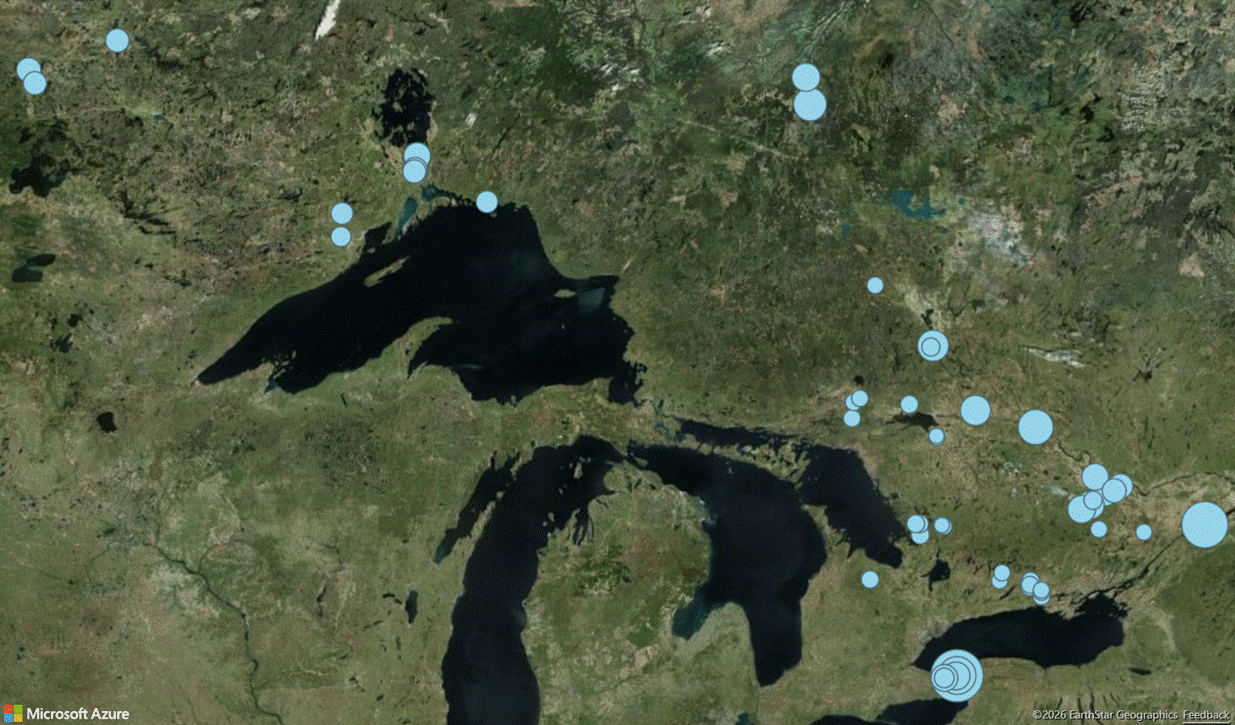

|

| Sites contracted under the HCI program |

The HCI was born out of a collapsing market price. The Energy Minister of the time, George Smitherman, directed the contracts to bail out generators whose revenue had dropped rapidly as 2008 came to an end in a time of declining natural gas prices and disappearing electricity demand – which was also the time of massive contracting of industrial wind and solar generators (at Smitherman’s direction). This was a welcome boon to small generators, such as the relatively local Orillia Power (who owned the dam and generator just upstream from where I am), and also to the larger companies that had bought facilities only a decade earlier as the government of that period (1995-2003) attempted to carve enough out of the body of the Ontario Hydro to generate some competition in a newly competitive marketplace. One big example: Brascan’s purchase of 490 MW of capacity at 4 sites on the Mississagi River in 2002. [i]

I’ll note two aspects of HCI contract-holders, many of which will apparently be NHP contract holders at a 20% lower rate: ownership is concentrated, with Brookfield (BRP Canada Corp.) accounting for 45% of the generating capacity, Great Lakes Power Ltd partnership [Algoma Hydro, Atlantis…] another 32%, and H2O Power another 12%. The other aspect is these are largely, and perhaps entirely, facilities originally built by the public Ontario Hydro – not the owners. At least 70% of the capacity is more than 50 years old (and perhaps as high as 98%).

After the introduction of the HCI, and the closure of coal-fired power plants in Ontario, the only remaining generating units exposed to the so-called market’s pricing were, Ontario Hydro remnant, OPG’s non-regulated hydroelectric generating stations. Parker Gallant and I described this in a May 2013 article in the Financial Post:

The big lag on OPG’s earnings has been the unregulated hydroelectric segment. It contributed more than $500-million or 46% of OPG’s pre-tax generation in 2008. Now it loses money. The reason for the loss is simple: OPG’s non-regulated hydro-electric assets are the only significant generation in Ontario exposed to the market price of electricity, which has collapsed under the McGuinty Liberal green energy manipulations. OPG’s non-regulated generation has fallen by 31% since 2008, revenue by 58%.

By the end of 2013 the government of the day had solved the problem, by regulating the price of all OPG’s hydro sites. At that point the IESO’s market had no participants actually exposed to the market price

One year ago the IESO implemented a renewed market construct, but the latest re-contracting initiative makes clear this market will not differ from the old in actually having market participants exposed to the market price – and certainly not by the appearance of merchant generator entrants betting on meeting the increased demand needs the government (and the IESO) are predicting.

The good news is the 20% lower pricing the IESO estimates the NHP will achieve, below the HCI generators current pricing (which I estimate are $116/MWh). The bad news is any impact of that on end-consumer pricing will be more than cancelled out as OPG has applied to jump its rates on regulated hydro production approximately 40%. While OPG starts from a much lower rate (~$47/MWh), it still begs the question: why are privately held legacy hydro stations getting cheaper while the public fleet gets far more expensive?

If this government and regulator won’t answer that question, the electorate should find somebody who will.

[initially posted to Cold Air substack]

[i] Brascan/Brookfield would be other sites, but these are the 4 currently listed as Brookfield’s under the latest IESO contract list. Notably the first summer of Brookfield’s ownership saw a “near draining of Rocky Island Lake,” on the Mississagi system. Contracts have since restricted the number of starts and stops at hydro sites.

No comments:

Post a Comment